How Firms Respond to Business Cycles: The Role of Firm Age and Firm Size

- Published: 27 August 2013

- Volume 61 , pages 520–559, ( 2013 )

Cite this article

- Teresa C Fort ,

- John Haltiwanger ,

- Ron S Jarmin &

- Javier Miranda

3432 Accesses

199 Citations

39 Altmetric

Explore all metrics

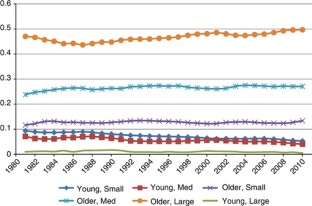

There remains considerable debate in the theoretical and empirical literature about the differences in the cyclical dynamics of firms by firm size. This paper contributes to the debate in two ways. First, the key distinction between firm size and firm age is introduced. The evidence presented in this paper shows that young businesses (that are typically small) exhibit very different cyclical dynamics than small/older businesses. The second contribution is to present evidence and explore explanations for the finding that young/small businesses were hit especially hard in the Great Recession. The collapse in housing prices accounts for a significant part of the large decline of young/small businesses in the Great Recession.

This is a preview of subscription content, log in via an institution to check access.

Access this article

Price includes VAT (Russian Federation)

Instant access to the full article PDF.

Rent this article via DeepDyve

Institutional subscriptions

Similar content being viewed by others

Bursting into life: firm growth and growth persistence by age.

Alex Coad, Sven-Olov Daunfeldt & Daniel Halvarsson

The heterogeneous dynamics between growth and profits: the case of young firms

Juan S. Federico & Joan-Lluis Capelleras

What does (not) characterize persistent corporate high-growth?

Stefano Bianchini, Giulio Bottazzi & Federico Tamagni

See evidence for the Kauffman Firm Survey, the Survey of Small Business Finance, and the Statistics of Business Owners.

Sharpe (1994) uses Compustat data from 1959 through 1985. Gertler and Gilchrist (1994) use the Quarterly Financial Report for Manufacturing Corporations , from 1958:4 through 1991:1. Chari, Christiano, and Kehoe (2007) extend the analysis in Gertler and Gilchrist (1994) to cover 1952:1 through 2000:3. Davis, Haltiwanger, Jarmin, and Miranda (2007) show the COMPUSTAT data are not representative of the economy as a whole.

Note that Moscarini and Postel-Vinay measure the net difference as the difference between large and small firms. In what follows, we use large/mature firms as the base so all of our differentials are for a group minus the large/mature firms. So in our analysis when we find a positive correlation, for example, between the net differential between old/small and large/older businesses with the unemployment rate, this is the same finding from that in Moscarini and Postel-Vinay. However, as will become clear we find the opposite pattern in our state-level analysis in response to state-specific cyclical shocks.

These authors use the U.S. Census Bureau Country Business Patterns data. These data provide geographic information about employment by establishment, not firm, size.

The BDS is built up from establishment-level data so we know the detailed geographic location of economic activity. The firm characteristics are based on the national firm but the state-level activity is for all establishments in that state in the given firm size and firm age group. The BDS is a public use database and can be downloaded from http://www.census.gov/ces/dataproducts/bds/index.html .

For a detailed description of differences between this and other sizing methodologies, see Haltiwanger, Jarmin, and Miranda (2013) . We include some analysis below and in the online appendix using firm size groups defined by initial size. Our results are robust to using this alternative.

If the age composition of establishments in the firm change due to M&A this does not change firm age.

This measure of net growth is bounded between (−2,2) and is symmetric around zero. Its desirable properties are discussed extensively in Davis, Haltiwanger, and Schuh (1996) .

Note that the level of aggregation “ s ” that we consider, it is not critical we use the DHS net growth rate at the cell level (for example, the log difference of E st and E st −1 yields very similar growth rates as the DHS net growth rate at this level of aggregation—this is not surprising since the DHS net growth rate is a second-order approximation to the log first difference). The advantage of the DHS net growth rate approach is the establishment entry and exit are readily integrated into the net growth rate measures.

The measurement appendix includes discussion and formulas that show how net and gross job flow rates are calculated for size and age groups.

Real GDP at the quarterly level is available at the national level so we construct annual averages using the retimed data. At the state level, real GDP can be constructed on an annual basis, but not for the properly retimed year. We use state GDP for robustness purposes, but note that it is off by quarter. We therefore also use real personal income at the state level which we can construct for the retimed year. Additional details are in the appendix .

As described in Decker and others (2013) , this is associated with a secular decline in the firm entry rate over this period of time. See that paper for more analysis and references to the literature on the secular decline in job flows observed over our sample period.

We also find that the employment shares by firm age and firm size classes are relatively stable at the state-year level which is the focus of much of our analysis.

These first two points echo the findings in Haltiwanger, Jarmin, and Miranda (2013) .

In unreported results, we have found that the job creation and job destruction patterns reflect consistent movements in the underlying components of job creation from continuers, job creation from entry, job destruction from continuers, and job destruction from exit. That is, all margins contribute to the patterns.

The online appendix can be found at http://www.palgrave.com/imfer/ .

The results in Haltiwanger, Jarmin, and Miranda (2013) and Foster, Haltiwanger, and Syverson (2012) show that the rich dynamics of young businesses extends through the first 10 years following entry. In our analysis, we restrict our attention to very young businesses in order to be able to track young businesses dynamics back to 1981. If we use the definition of young businesses as being 10 years or less then we would have to restrict our analysis to commence in 1987. But it is clear that young businesses so defined contribute very substantially to cyclical dynamics of employment.

Table A.1 of the online appendix presents simple descriptive regressions that show that all groups’ net growth is procyclical, with young/small businesses being especially procyclical.

Moscarini and Postel-Vinay (2012) also note that their result is only robust to considering cyclical indicators based on deviations from trend and not robust to using cyclical indicators of expansions or contractions. We find that when the latter indicators are used, young/small and young/medium businesses are more cyclically responsive than older/large businesses. Moscarini and Postel-Vinay (2012) use initial firm size to classify firms in their analysis. In Table A.2 of the online appendix , we show the results of Table 1 are robust to this alternative so this is not driving differences. Moreover, in Table A.5 of the online appendix we show that the state by year patterns emphasized in our subsequent analysis are robust to using initial firm size to classify firms. We also show in Figure A.2.7 that the impulse responses to state-specific cyclical and housing price shocks are robust to using initial size to classify firms.

One way to emphasize that there is an inherent difference between considering firm size and firm age effects is simply to consider correlations where one focuses on only firm age effects and those where one only focuses on firm size effects. We find that if we use only firm age and consider two age groups where young is <5 and mature is 5+ that the correlation between the change in unemployment rate and the net differential between young and mature is −0.65 (and significant). In contrast, if we only consider firm size with two size groups where small/medium is <500 and large is 500+ (and to be similar to Moscarini and Postel-Vinay use initial size classification), then the correlation between the change in the unemployment rate and the net differential between small/medium and large is −0.26 and not significant. Turning to the indicator used by Moscarini and Postel-Vinay we find that the latter correlation is 0.36 and significant. The latter differs some from the correlation emphasized by Moscarini and Postel-Vinay (recall they have the opposite sign convention and so this is equivalent to a −0.36 correlation with their sign convention). We find that this is associated, at least in part, with the specific time-series sample. That is, if we use the 1981–2009 sample (closer to what Moscarini and Postel-Vinay use), we obtain a correlation between the HP filtered unemployment rate and the net differential between small and large of 0.54 which is very similar to their highlighted correlation. Simply adding/subtracting one year alters this correlation nontrivially.

Even using the HP-filtered unemployment rate, the young-small differential with old-large is smaller in magnitude than the old-small differential with old-large. The implication is that young-small are more cyclically sensitive than old-small even with the HP-filtered unemployment rate.

We also show in Table A.5 that the results in Table 2 are robust to using initial size.

Like the results in Table 2 , we also find that older/small businesses are less cyclically sensitive than young/small businesses as the coefficients are substantially smaller in magnitude for the older/small businesses. But we find that even older/small businesses respond more to the state-specific component of this indicator than large/older businesses (although the estimate for the old/small differential is only significantly different from zero at the 10 percent level).

We note that Moscarini and Postel-Vinay (2012) also consider state-level variation. Unlike our analysis, they did not control for state and year effects. We show in Table A4 of the online appendix that the results in Table 2 using the change in the unemployment rate are robust to not controlling for year effects for young/small and young/medium net differentials. However, in Table A4, we find that estimated effect for the old/small differential with old/large turns positive and significant when controlling only for state fixed effects. Moreover, in unreported results, we find that when we don’t control for year effects but do control for state effects and use the HP filtered unemployment rate that we obtain the Moscarini and Postel-Vinay result for old/small net differentials with large/old businesses but don’t find their result for small/young net differentials. Thus, our findings suggest that their results are being driven by old/small businesses relative to old/large and by aggregate variation in their measure and not by state-specific variation in their measure. We also note that in all of these alternative specifications, we always find that young/small businesses are more sensitive to housing price shocks. We find this for the descriptive regressions as well as the panel VAR analysis regardless of the cyclical indicator we use.

We thank Inessa Love for her STATA code (pvar.ado) to implement a panel VAR procedure in STATA. We have modified the code for our application (code available upon request). Consistent with Love and Zicchino (2006) (building on the insights of Arellano and Bover, 1995 ) we use the Helmert transformation to control for state fixed effects. This forward differencing procedure overcomes the problem that fixed effects and lagged dependent variables are inherently correlated.

The results using the net employment growth rate are in Figures A.2.1–A.2.3, for the HP filtered unemployment rate in Figures A.2.4–A.2.5, for real GDP growth in A.2.14–A.2.16 and for real Personal Income in A.2.17–A.2.19.

Their approach to identification is to instrument the local leverage ratio with the housing supply elasticity from Saiz (2010) . Our approach is to use the panel VAR with the Cholesky decomposition to identify a housing price shock that is orthogonal to general business conditions in the state.

As is typical in the identification of idiosyncratic shocks, it is difficult to distinguish between a true idiosyncratic shock and an idiosyncratic response to a common shock.

See Figures A.2.6.a and A.2.6.b in the online appendix .

We also note that examination of the impulse response functions with respect to these net differential shocks shows only modest dynamic impact on the change in unemployment and housing price growth.

All figures include 95 percent confidence bands.

We show in Online Appendix Figure A.2.12 that we obtain our main results if we focus only on firm age (ignoring firm size) so that we focus on the net differential between young and mature. In Appendix Figure A.2.13 , we show that if we instead had focused on firm size only (ignoring firm age) we would obtain substantially mitigated effects of both the local cyclical shock and the local housing price shock. These results are a way of emphasizing that the critical factor for obtaining our results is to distinguish across firms by firm age and not firm size. A simple way of thinking about this and consistent with the results throughout the paper is that young firms are small and medium size (essentially no young/large firms) whereas small firms are both young and mature. The results throughout the paper show that old/small firms behave quite differently than young/small and young/medium firms.

An additional calculation of interest for the upper bound estimates is the overall fraction of the decline in the net differential for young/small that can be accounted for housing prices in the 2007–09 period. Weighting the states by employment, the average overall contribution is 60 percent. Note that this calculation is not applicable for the baseline estimates with year effects since by construction with year effects the average overall effect in any given year from state-specific variation in housing prices is zero. That is, in the baseline specification we are focusing on identifying and accounting for state-specific variation in the net differentials. We focus on the latter in Table 4 and in the accompanying discussion.

It would be of interest to highlight the difference in the role of housing prices in the 2007–09 recession relative to the 1981–83 recession. Our sample period is from 1981–2010 and we exploit variation from the 1981–83 period in our estimation but with a panel VAR with two years of lags our first period of predicted values is in 1983. Note that we start our sample in 1981 given that the LBD starts in 1976 and our focus on identifying the contribution of young businesses. Given left censoring in firm age, we can consistently measure the contribution of young firms less than five years old and five years or more from 1981.

Analogous to the concerns expressed for the analysis of job creation and job destruction, one concern in comparing results across specifications that differ by sector is that the identified state cyclical shocks and housing price shocks and their respective dynamics vary across specifications. In practice, each of these sectoral specifications yields very similar state-specific cyclical shocks and state-specific housing price growth shocks.

In unreported results, we have explored the net responses of all groups rather than the net differential responses to cyclical and housing price shocks. We find that all firm size/age groups in all sectors experience a decline in net employment growth in response to an increase in the state-specific unemployment rate. Consistent with our findings, we find that the magnitude of the response is largest for the young/small firms. The point is that the net differential responses are associated with all firm size and age groups experiencing a decline in local cyclical downturns but young/small experiencing the larger and that this pattern holds for all sectors. In response to housing price shocks, similar remarks apply but with the largest magnitude being for the young/small in the Construction, Retail Trade, FIRE and Service sectors.

Adelino, Schoar, and Severino (2013) similarly find smaller effects in these sectors and suggest this is consistent with a financial transmission channel for home equity.

Pushing on this point further, our housing price shocks are orthogonal to the local cyclical shock. If the latter captures changes in local aggregate demand, then the variation in housing prices we exploit is orthogonal to local demand effects. We note that, in this regard, our results are robust to using a variety of indicators of local cyclical conditions including real GDP growth and real Personal Income growth.

Adelino, Manuel, Antoinette Schoar and Felipe Severino, 2013, “House Prices, Collateral and Self-Employment,” mimeo .

Aghion, Philippe and Peter Howitt, 2006, “Appropriate Growth Policy: A Unifying Framework,” Journal of European Economic Association, Vol. 4, No. 2–3, pp. 269–314.

Article Google Scholar

Arellano, M. and O. Bover, 1995, “Another Look at the Instrumental Variable Estimation of Error Component Models,” Journal of Econometrics, Vol. 68, No. 1, pp. 29–51.

Chari, V.V., L. Christiano and P. Kehoe, 2007, “The Gertler-Gilchrist Evidence on Small and Large Firm Sales,” mimeo .

Davis, Stephen J. and John Haltiwanger, 2001, “Sectoral Job Creation and Destruction Responses to Oil Price Changes and Other Shocks,” Journal of Monetary Economics, Vol. 48, No. 3, pp. 465–512.

Davis, Stephen J., John Haltiwanger, Ron Jarmin and Javier Miranda, 2007, “Volatility and Dispersion in Business Growth Rates: Publicly Traded versus Privately Held Firms,” NBER Chapters, in NBER Macroeconomics Annual 2006, Vol. 21, ed. by D. Acemoglu, K. Rogoff and M. Woodford (National Bureau of Economic Research, Inc.), pp. 107–80.

Google Scholar

Davis, Stephen J., John Haltiwanger and Scott Schuh, 1996, Job Creation and Destruction (Cambridge, MA: MIT Press).

Decker, Ryan, John Haltiwanger, Ron Jarmin, and Javier Miranda, 2013, “The Secular Decline in Business Dynamism in the U.S.”, mimeo .

Ericson, Richard and Ariel Pakes, 1995, “Markov-Perfect Industry Dynamics: A Framework for Empirical Work,” Review of Economic Studies, Vol. 62, No. 1, pp. 53–82.

Foster, Lucia, John Haltiwanger, and Chad Syverson, 2012, “The Slow Growth of New Plants: Learning about Demand,” NBER Working Paper No. 17853.

Gertler, Mark and Simon Gilchrist, 1994, “Monetary Policy, Business Cycles, and the Behavior of Small Manufacturing Firms,” The Quarterly Journal of Economics, Vol. 109, No. 2, pp. 309–40.

Haltiwanger, John, 2013, “What is the Contribution of Entrepreneurs to Jobs and Productivity?,” mimeo .

Haltiwanger, John, Ron Jarmin, and Javier Miranda, 2013, “Who Creates Jobs? Small vs. Large vs. Young,” Review of Economics and Statistics, Vol. 95, No. 2, pp. 347–61.

Holtz-Eakin, Douglas, Whitney Newey, and Harvey S. Rosen, 1988, “Estimating Vector Autoregressions with Panel Data,” Econometrica, Vol. 56, No. 6, pp. 1371–95.

Hopenhayn, H, 1992, “Entry, Exit, and Firm Dynamics in Long Run Equilibrium,” Econometrica, Vol. 60, No. 5, pp. 1127–50.

Hurst, Erik and Anna Maria Lusardi, 2004, “Liquidity Constraints, Household Wealth, and Entrepreneurship,” Journal of Political Economy, Vol. 112, No. 2, pp. 319–47.

Hurst, Erik and Benjamin Pugsley, 2012, “What Do Small Businesses Do,” Brookings Papers on Economic Activity, Vol. 43, No. 2 (fall), pp. 73–142.

Jovanovic, B, 1982, “Selection and the Evolution of Industry,” Econometrica, Vol. 50, No. 3, pp. 649–70.

Love, Inessa and Lea Zicchino, 2006, “Financial Development and Dynamic Investment Behavior: Evidence from panel VAR,” The Quarterly Review of Economics and Finance, Vol. 46, No. 2, pp. 190–210.

Lucas, R.E., 1978, “On the Size Distribution of Business Firms,” The Bell Journal of Economics, Vol. 9, No. 2, pp. 508–23.

Melitz, M., 2003, “The Impact of Trade on Intra-industry Reallocations and Aggregate Industry Productivity,” Econometrica, Vol. 71, No. 6, pp. 1695–726.

Mian, Atif and Amir Sufi, 2010, “Household Leverage and the Recession of 2007–09,” IMF Economic Review, Vol. 58, No. 1, pp. 74–116.

Mian, Atif and Amir Sufi, 2011, “House Prices, Home Equity-Based Borrowing, and the U.S. Household Leverage Crisis,” American Economic Review, Vol. 101, No. 6, pp. 2132–56.

Mian, Atif and Amir Sufi, 2012, “What Explains High Unemployment? The Aggregate Demand Channel,” mimeo .

Mishkin, Frederic S., 2008, “Small Business Lending,” Testimony before the Committee on Small Business and Entrepreneurship, U.S. Senate, April 2008.

Moscarini, Guiseppe and Fabien Postel-Vinay, 2012, “The Contribution of Large and Small Employers to Job Creation in Times of High and Low Unemployment,” American Economic Review, Vol. 102, No. 6, pp. 2509–39.

Robb, Alicia and David Robinson, forthcoming, “The Capital Structure Decisions of Startup Firms,” Review of Financial Studies.

Saiz, Albert Saiz, 2010, “The Geographic Determinants of Housing Supply,” Quarterly Journal of Economics, Vol. 125, No. 3, pp. 1253–96.

Sharpe, Stephen, 1994, “Financial Market Imperfections, Firm Leverage, and the Cyclicality of Employment,” American Economic Review, Vol. 84, No. 4, pp. 1060–74.

Syverson, Chad, 2011, “What Determines Productivity?” Journal of Economic Literature, Vol. 49, No. 2, pp. 326–65.

Tornqvist, Leo, Pentti Vartia, and Yrjo Vartia, 1985, “How Should Relative Changes Be Measured?” American Statistician, Vol. 39, No. 1 (February), pp. 43–46.

Download references

You can also search for this author in PubMed Google Scholar

Additional information

Supplementary Information accompanies the paper on the IMF Economic Review website (www.palgrave-journals.com/imfer)

* Teresa Fort is an Assistant Professor at the Tuck School at Dartmouth College. John Haltiwanger i4s a Distinguished Unirsity Professor at the Universi5y of Maryland. Ron Jar5in is Assistant Director for Res6arch and Methodology at the U.S. Census Bureau. Javier Miranda is a Principal Economist at the U.S. Census Bureau. The authors thank participants at seminars at CES, Harvard, and INSEAD, FRB, Bank of Spain, attendees at the IMF ARC Conference and the NBER Entrepreneurship Workshop, Pierre-Olivier Gourinchas, Roberto Fattal Jaef, Ayhan Kose, Giuseppe Moscarini, Johannes Schmeider, Robert Strom, and two anonymous referees for helpful comments, and the Kauffman Foundation for financial support. Any opinions and conclusions expressed herein are those of the authors and do not necessarily represent the views of the U.S. Census Bureau. All results have been reviewed to ensure that no confidential information is disclosed. The authors thank Ryan Decker for his assistance in developing the STATA code used in this paper as well as Inessa Love for the original version of PVAR.

Electronic supplementary material

Online appendix, work files for online appendix, measurement and data appendix, measurement of net and gross job flows.

Our measures are taken from the Business Dynamic Statistics (BDS). The net job creation and gross job flow measures are based on the methodology of Davis, Haltiwanger, and Schuh (1996) . In the BDS, establishments are classified by their parent firm’s size and firm age. This is based on the parent firm for the establishment. Firm size is available using both current average size (the average size of the parent firm in the prior and current year) and initial size (the size of the parent firm in the prior year). Firm age is based on the age of the oldest establishment when a new firm is started and then ages naturally thereafter. It is based on the parent firm in the current year. As noted in the text we collapse the available firm size and firm age categories into broad firm size and firm age categories. For any given cell “ s ” defined by a firm size and firm age category is equal to:

where E st is employment for cell “ s ” in period t , X st =0.5 × ( E st + E st −1 ). Footnote 39 . In measuring and defining E st −1 , it is critical to emphasize that this is the employment in period t −1 of the establishments that are in cell “ s ” in period t . That is, this is based on the same set of establishments in period t −1 and t (and this is not subject to the “size distribution fallacy” discussed in Davis, Haltiwanger, and Schuh (1996) wherein misleading inferences can be generated by considering cell-based totals of establishments classified by firm size (or firm age) across years as establishments can change firm size and firm age classifications). Another way of making this point is to note that the growth rate for the cell can be equivalently generated by:

The net growth rate for the cell can be decomposed into the contribution of job creation and destruction as follows. Define job creation and job destruction for the cell as:

By construction, net employment growth for the cell can be decomposed into:

Note that the cells for young firms include establishments of new firms (firm age=0). All such establishments have DHS net growth rates at the establishment level equal to 2. For the young firm cell, when there is a decrease in the share of young firm employment accounted for by new firms, the cell-based growth rate will decline. But the net growth rate for the young firm cells will also reflect the job creation of firms older than firm age=0 as well as the job destruction of firms older than firm age=0.

Cyclical Variable Construction

Unemployment rate : The national unemployment rate is based on quarterly data from the Bureau of Labor Statistic’s (BLS) Current Population Survey for 1979–2010. The state-level unemployment data are also quarterly and come from the BLS regional and state-level data releases available on FRED. We construct yearly data for the regression analysis by averaging the unadjusted, quarterly data over the retimed year. We calculate the yearly change as: δ U t = U t − U t −1 , where t represents the re-timed year. We also HP filter the unemployment as an alternative measure that captures deviations from the long-term trend.

Real GDP and Real Personal Income : Quarterly Real GDP at the national level is readily available from the BEA (Real GDP is nominal GDP deflated by the GDP implicit price deflator). We take time averages for the retimed year and compute log first differences. At the state level, nominal GDP is available on an annual basis but not for the retimed year. As the re-timed year is only off by a quarter, we use this in our analysis with appropriate caution. We deflate the state-level nominal GDP with the national implicit price deflator and then compute growth rates with log first differences. At the state level, a related alternative measure is available quarterly—personal income. The latter is income from all sources available to households. We deflate the latter on a quarterly basis with the national implicit price deflator, take averages for the retimed year, and then compute growth rates with log first differences.

Housing Prices : The housing price measure is based on the FHFA House Price Index. The HPI is a weighted, repeat-sales index. It measures the average price changes in repeat sales or refinancings on the same properties. The information for the HPI is obtained from repeat mortgage transactions on single-family properties whose mortgages have been purchased or securitized by Fannie Mae or Freddie Mac since January 1975.

We use unadjusted HPI data that are quarterly, by state. We divide the HPI by the BLS Urban Consumer Price Index for all items so that the data are in real terms. We then average the quarterly index over the retimed year and calculate the log first difference in home prices.

Rights and permissions

Reprints and permissions

About this article

Fort, T., Haltiwanger, J., Jarmin, R. et al. How Firms Respond to Business Cycles: The Role of Firm Age and Firm Size. IMF Econ Rev 61 , 520–559 (2013). https://doi.org/10.1057/imfer.2013.15

Download citation

Published : 27 August 2013

Issue Date : 01 August 2013

DOI : https://doi.org/10.1057/imfer.2013.15

Share this article

Anyone you share the following link with will be able to read this content:

Sorry, a shareable link is not currently available for this article.

Provided by the Springer Nature SharedIt content-sharing initiative

JEL Classifications

- Find a journal

- Publish with us

- Track your research

Academia.edu no longer supports Internet Explorer.

To browse Academia.edu and the wider internet faster and more securely, please take a few seconds to upgrade your browser .

Enter the email address you signed up with and we'll email you a reset link.

- We're Hiring!

- Help Center

Firm Age and Financial Performance: The Firm Life-Cycle Theoretical Perspective of Private Limited Companies In Uganda

International Journal of Business Strategies

Purpose: While the financial performance of private companies has invoked intense interest globally, this study aimed to investigate the relationship between firm age and the financial performance of private limited companies in Uganda. Methodology: The study adopted a positivist paradigm and a cross-sectional design. A structured self-administered questionnaire was deployed to gather quantitative data from Accountants, Auditors, CEOs, and Board Members who were purposively selected. Three hundred ninety-four private companies in Central and Western Uganda were sampled. The relationship was assessed using Pearson correlation and standard regression analysis techniques. Findings: The study established a positive relationship between firm age and financial performance. It was established that firm age accounts for 14% of the variance in financial performance among private limited companies in Uganda. The study recommends that managers prioritize factors that guarantee the long-term ex...

Related Papers

International Journal of Academic Research in Business and Social Sciences

Samuel Pule

Journal of Global Economics, Management and Business Research

DR. OMALIKO EMEKA LEONARD. FSASS, AISDS

The study examined the effect of corporate life cycle on financial performance of listed industrial goods firms in Nigeria. Corporate life cycle was proxy with; firm introductory stage (FINT), firm growth stage (FGRT), firm maturity stage (FMAT), firm shakeout stage (FSHK) and firm decline stage (FDEC) while financial performance was proxy using net assets per share. Ex Post Facto Design was adopted and data for the study were collected from the annual reports and accounts of the listed industrial goods firms in Nigeria for the period ended 2017-2021. Panel least squares model was used in the data analysis and the findings of the study indicate that there is a significant and positive relationship between firm growth stage, firm maturity stage, firm shakeout stage and financial performance of industrial goods firms in Nigeria at 1% significant level while firm introductory stage and firm decline stage have insignificant relationship with financial performance. Thus, the study concludes that corporate life cycle ensures financial performance of listed industrial goods firms in Nigeria. The study recommends that managers should have a focus on board monitoring and financial management accordingly and especially during maturity stage so as to avoid slipping into the next stage, which is restructuring stage or decline stage.

The study examined the effect of corporate governance on firm's financial performance amongst private business enterprises in Uganda. The study used descriptive and survey design. A mixed method approach which involved both qualitative and quantitative techniques were also used. The study found out that corporate governance significantly influences the financial performance of hotels and manufacturing firms in Lira City and majority of the firms investigated performed on average financially. It was also established that firms whose boards demonstrate high integrity were likely to register positive changes in their financial performance than firms whose boards do not. The study also noted that board independence would propel the firm to grow to greater heights. The study recommends that hotel and manufacturing firm owners should exercise some discipline and leave boards to operate independently. This would allow the board to remain focused on the long-term goals of the firm. The hotel and manufacturing firm owners should be cautious in selecting board members lest they attract many that would increase the firm's liabilities.

Nixon Kamukama

Purpose: The study aimed at examining the relationship between board composition and financial performance of private limited companies in Uganda. Methodology: A positivist approach and a cross-sectional research design were employed to collect data from 394 companies in Central and Western Uganda. An open-ended questionnaire was used to collect data from board members and executives from companies. Pearson correlation and standard linear regression were employed for data analysis. Findings : Results indicate a positive relationship between non-executive directors on the Board and the financial performance of private companies. Unique Contribution to practice and policy : Private Limited Companies in Uganda will attain the much-desired insights in the context of how board composition links with their financial performance. The study recommends the management`s careful consideration of long survival prospects as well as the formulation of appropriate policies and survival strategies ...

iqbal khurshed

American Journal of Finance

Nimusiima Pereez , Wilbroad Aryatwijuka , Rwakihembo John

Purpose: This study aimed to establish the association between the board leadership structure and the financial performance of private limited companies in Uganda. Methodology: The study adopted a positivist paradigm and a cross-sectional design. 394 private companies were sampled from Central and Western Uganda. Quantitative data were collected from board members, accountants, auditors, and CEOs using a self-administered structured questionnaire. Pearson correlation and standard regression analyses were conducted for data analysis. Findings: The study established a positive relationship between a separate leadership structure and the financial performance of private companies. Separate leadership was confirmed as a recipe for private companies' financial success, accounting for 7% of the variance. The study also revealed that CEO duality was common amongst most private limited companies in Uganda. Unique Contribution to Practice and Policy: The study calls for a re-examination ...

khisa kodia

Abstract Venturing into business is thought to play an important role particularly to retirees as a source of extra income and also for keeping themselves busy in retirement. However, in spite of efforts from various stakeholders to enhance success of the retirees’ businesses, they have been performing poorly. According to the Retirement Benefits Authority (RBA) most businesses started by retirees fail within the first three years. The main objective of the study was to examine the factors affecting the performance of businesses of public corporation retirees in Kisumu. The study used a sample size of 193 retirees, who were picked from a population of 642 through stratified sampling technique. The study was a descriptive survey of the retirees and used both primary and secondary data. Primary data was collected from relevant retirees using structured questionnaires. Secondary data was obtained from the institutional reports and records of the retirees. The data collected was analyzed using descriptive statistics and presented in form of tables and frequency distributions. This study revealed that the major factors affecting performance of retirees’ businesses include financial stability, physical and mental strength, entrepreneurial skills and family base, which accounted for significant failure of businesses of retirees of public corporations in Kisumu. It was also revealed that many retirees lacked proper human relations skills to motivate and retain internal customers (employees) as well as maintain consistently satisfied customers. The study recommended that retirees in business should endeavour to attend trainings/seminars to improve their business and financial management skills. Further, the study recommended the enactment of a compulsory pre-retirement training on financial and business management for employees with at least five years to retirement. The researcher suggested that a similar study be done focusing on external factors affecting business performance and also focus on retirees in the private sector. Key words: Business performance, entrepreneurship, public corporations, pre-retirement planning, retirement benefits, retiree, Retirement Benefits Authority.

D. Shahimi , Muhammad Arafat Noordin

IOSR Journals

Background: The aim of this study was to determine the effect of the marketing mix (7P) consisting of Products, Prices, Promotions, Places, People, Processes, and Physical Evidence on the decision making process of tourists visiting in Makassar. This study is a quantitative study using a total sampling of 101 respondents with non-probability sampling methods. The research analysis technique used in this study is a multiple regression analysis to determine the relationship between variables obtained from previous studies or from references.The results shown that all variables used simultaneously affect the Purchase Decision. The hypothesis which explains that the variable Services Marketing Mix simultaneously influences the Purchasing Decision is accepted.The R Square is 0.323 or 32.3%. That is, the marketing mix variable used in this study simultaneously affected purchasing decisions by 32.3% while the remaining 67.7% was influenced by other variables outside this regression equation or variables not examined.The test also shows how the partial effect of each variable on the Purchasing Decision. The results when doing the t test obtained the results that only the Price (X2) and Location (X4) have a positive and significant effect on Purchasing Decisions. So in other words that the hypothesized variable Services Marketing Mix partial effect on Purchasing Decisions is rejected.

Michael Wyss

RELATED TOPICS

- We're Hiring!

- Help Center

- Find new research papers in:

- Health Sciences

- Earth Sciences

- Cognitive Science

- Mathematics

- Computer Science

- Academia ©2024

IMAGES

VIDEO

COMMENTS

217. THE IMPACT OF AGE ON FIRM PERFORMANCE: A LITERATURE REVIEW. Matteo Rossi*. *University of Sannio, Italy. Abstract. In the last thirty years t he link b etween firm age and performance has ...

This Special Issue on "Firm Age and Performance" seeks to collect evidence on the effect of firm age on performance and make it available collectively. The special issue starts with a review of the literature (Coad 2017) which is then followed by six empirical studies on the relationship between firm age and innovation (Pellegrino 2017 ...

Literature review — firm growth-profitability dynamics and the role of age and size. The theoretical approaches to whether growth drives profit or profitability, or vice versa, ... Inspired by previous findings on firm age (Ben-Hafaïedh and Hamelin, 2022; Steffens et al., ...

Innovation, firm growth, and the moderating effect of firm age: A literature review. While some studies have focused on how innovation changes with age, other studies - more closely related to our present paper - focus on how age moderates the ways in which firms benefit from innovation. In fact, the empirical literature has found both ...

Amid increasing interest in firm age and its effects on firm performance, this special issue offers an exhaustive review of the literature and a novel collection of evidence on the effects of firm age on performance, including a special focus of interest on innovation performance, financial performance, exports, survival and growth. This editorial positions the theme in the extant literature ...

In the last thirty years the link between firm age and performance has fascinated a lot of scholars. In fact, since 1990 there has been a major attention on management studies on this topic. But the debate on this theme have produced mixed results, which resulted in extensive economics discussion, albeit without a systemic vision. The firm age literature has not yet developed a paradigm.

The literature suggests that firm age can also influence the relationship between asset tangibility and debt and firm age can negatively moderate the relationship between asset tangibility and leverage for several reasons. Firstly, older firms may have a higher proportion of depreciated or obsolete assets, which may potentially lessen the ...

We survey the literature on firm age in an attempt to improve our understanding of firms of different ages - to better understand how firm behaviour and performance relates to the demographics of the business population. ... Organizational routines: a review of the literature. Ind Corp Chang 13(4):643-677. Article Google Scholar Becker MC ...

Corporate Ownership & Control / Volume 13, Issue 2, Winter 2016, Continued -1. 217. THE IMPACT OF AGE ON FIRM PERFORMANCE: A LITERATURE REVIEW. Matteo Rossi*. *University of Sannio, Italy. Abstract. In the last thirty years the link between firm age and performance has fascinated a lot of scholars.

With regards to the firm age, the interest in this variable began to grow in parallel with the studies that included firm age as an explanatory factor in investigations of determinants of firm performance i.e. business success. ... Our empirical literature review shows that little is known about how firm performance changes with age, presumably ...

The firm age literature has not yet developed a paradigm. Starting to a simple question: "age benefits performance?", the purpose of this paper is to present a systematic review of the existing literature. The critical examination of the relation between firm age and performance provides new insights for executives.

Literature Review While some theoretical models considered the firm size as linearly related to firm age (Greiner, 1972), the others postulated specific predictions regarding the influence of firm age on its performance. Coad et al. (2013) summarized these predictions in three categories: selection effects, learning-

Our paper contributes to the literature by examining the effects of firm age on how corporate governance influences a firm's capital structure choices after explicitly addressing the aforementioned empirical concerns. To do this, we use data on U.S. corporations from 1996 to 2016.

Abstract. Our empirical literature review shows that little is known about how firm performance changes with age, presumably because of the paucity of data on firm age. For Spanish manufacturing ...

Literature Review 2.1 Firm Age There are many ways used by previous researchers to measure firm age; depending on the objective of their study. Morgan, Kaleka and Katsikeas (2004) defined firm age in terms of the number of years firm has been engaged in exporting operations whilst Ainuddin, Beamish, Hulland and Rouse (2007) used the age of ...

The critical examination of the relation between firm age and performance provides new insights for executives. Keywords: Firm Age, Longevity, Old Firms, New Firms, Innovation Performance, Financial Performance, Organizational Impact. How to cite this paper: Rossi, M. (2016). The impact of age on firm performance: A literature review.

Although this review of the firm dynamics literature has been necessarily brief, it does highlight that young/small businesses are likely to be quite different from old/small businesses. ... Firm age in the BDS is based on the age of the oldest establishment of the firm when the firm is created. For firm startups—firms with all new ...

LITERATURE REVIEW AND HYPOTHESIS DEVELOPMENT Firm Profitability According to Ilaboya (2016), "profitability is the level of profit in relation to the volume of ... firm age and profitability, the older a firm is, the more productive and less profitability it would be. While in the study conducted by Ilaboya (2016), a significant relationship ...

Firm Size, Age… 49 ISSN: 2635-2966 (Print), ISSN: 2635-2958 (Online). ... review extant literature and develop hypotheses in section two. Section three addresses the study methodology with emphasis on analytical review and model specification. Section four presents the

Empirical Literature Review Firm Age and Financial Performance Whereas some theoretical models and empirical studies (Busse et al., 2020; Ryu & Won, 2022; Akbar et al., 2019; Yang et al., 2022) consider firm age to be linearly related to financial performance, scholars postulate contradicting findings concerning the direction of the relationship.

Other studies also investigated the company president age and found close results. Belenzon et al. (2019), when studying companies in France, Italy, and United Kingdom, found that CEOs average age ...

Extant literature suggests that a firm's financial performance is a function of its age, and this relationship is supported by the firm life-cycle theory ( Can et al., 2023 ). According to this ...