Join 307,012+ Monthly Readers

Get Free and Instant Access To The Banker Blueprint : 57 Pages Of Career Boosting Advice Already Downloaded By 115,341+ Industry Peers.

- Break Into Investment Banking

- Write A Resume or Cover Letter

- Win Investment Banking Interviews

- Ace Your Investment Banking Interviews

- Win Investment Banking Internships

- Master Financial Modeling

- Get Into Private Equity

- Get A Job At A Hedge Fund

- Recent Posts

- Articles By Category

Investment Banking Pitch Books: Design, Examples & Templates

If you're new here, please click here to get my FREE 57-page investment banking recruiting guide - plus, get weekly updates so that you can break into investment banking . Thanks for visiting!

Bankers like to complain about almost everything, but near the top of the complaint list is “investment banking pitch books.”

Some Analysts claim that you’ll devote all your waking hours to creating these documents, while others say they’re time-consuming but not that terrible to create.

Some senior bankers swear by pitch book presentations, claiming that they help to win and close deals, while others think they’re over-hyped.

We’ll look at all those points and more in this article, including downloadable pitch book examples and templates for you to use.

Table Of Contents:

- What Is An Investment Banking Pitch Book?

How to Create a Pitch Book

Pitch book presentation, part 1: pitching your team as the advisor of choice, pitch book presentation, part 2: providing background and context, pitch book presentation, part 3: choose your own adventure, sell-side pitch books for sell-side mandates, buy-side pitch book examples, equity pitch book and debt pitch book examples for financing mandates, other types of pitch books, why do you spend so much time on investment banking pitch books as a junior banker, what do you need to know about pitch books as an intern or new hire, what is an investment banking pitch book.

Pitch Book Definition: In investment banking, pitch books refer to sales presentations that a bank uses to persuade a client or potential client to take action and pay for the bank’s services. Pitch books typically contain sections on the merits of the transaction; analysis of potential buyers or sellers; pricing and valuation information; as well as key risks to mitigate.

That is the classic definition, but in practice, people use the term “pitch book” to refer to almost any presentation created by a bank.

We’re going to focus on presentations to potential clients here because they tend to be the most time-consuming ones, and they generate the most horror stories as well.

There’s no way to “measure” how much pitch books matter, but it’s safe to say that they’re less important than the time spent on them implies.

Bankers win deals primarily because of relationships cultivated over a long time ; a pretty presentation right before a company goes public means little compared with the 5-10 years of meeting the CEO and CFO before that point.

Pitch books matter to you as an investment banking analyst or associate primarily because you’ll spend a good amount of time creating them – and you can’t screw up if you want a good bonus .

Almost all investment banking pitch books use a structure similar to the following:

- Situation, 0r “Current State”: Your prospective client is looking for growth.

- Complication, or “Problem”: The potential client’s growth rate has been slowing down.

- Hypothesis, or “Solution”: Acquiring a growing company can meet the potential client’s need for growth.

Then, you go into detail showing why the hypothesis might be true – including why your team is qualified to lead this transaction, similar transactions you’ve led before, and the valuation this company can expect to receive.

Investment Banking Pitch Book Sample PPT and PDF Files and Downloadable Templates

Here are a number of example pitch books in editable Powerpoint (PPT, PPTX) and PDF versions, drawn from some of the case studies within our investment banking courses :

- Jazz Pharmaceuticals – Valuation and Sell-Side M&A Pitch Book (PPT)

- Jazz Pharmaceuticals – Valuation and Sell-Side M&A Pitch Book (PDF)

- KeyBank and First Niagara – FIG M&A Pitch Book (PPT)

- KeyBank and First Niagara – FIG M&A Pitch Book (PDF)

- Netflix – Equity, Debt, and Convertible Bond Financing Pitch Book (PPT)

- Netflix – Equity, Debt, and Convertible Bond Financing Pitch Book (PDF)

Here’s what you can expect in the first few parts of any pitch book, including many examples from actual bank presentations:

The first section of investment banking pitch books introduces your firm’s platform, recent transactions, and team.

You might include stats on your firm’s position in the league tables , or explain its growth story and how it’s different from its competitors. Here are a couple of examples:

You might also write about distribution partnerships and other strategic developments here.

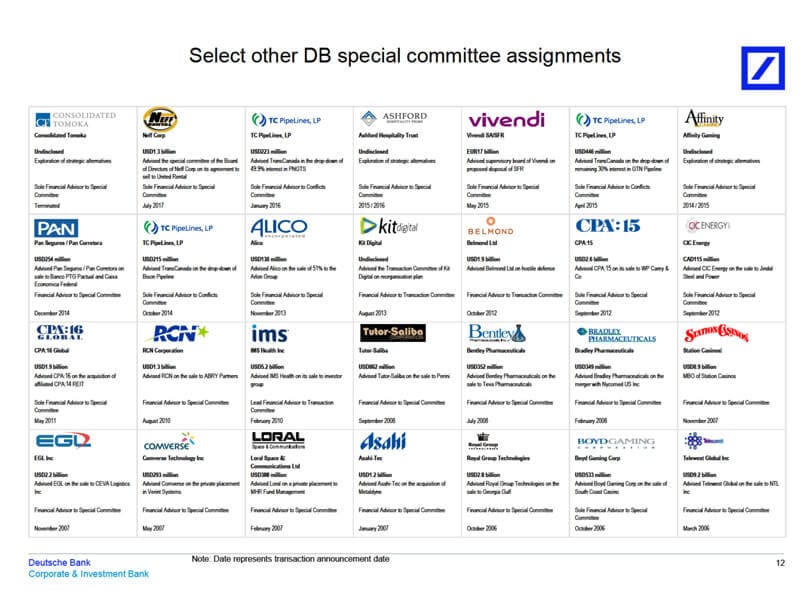

The next section consists of credentials , which include similar transactions your team has completed. Since turnover at banks is high, these lists often include transactions completed by team members when they were at other banks.

Here are a few examples:

These pages look simple, but they can be time-consuming to put together because you need to find the most relevant deals and rearrange elements from other presentations.

You may also go into more detail on a few deals and devote entire pages to them.

Banks often call these 1-page descriptions “ case studies ,” and you can see a few examples below:

Finally, this section will include a team biography , including previous firms, relevant deals/clients, and education for each member:

Before you move into the specific situation of the company you’re meeting, you’ll usually share some updates on the industry as a whole and recent deal activity in the sector.

Unlike the first part, which was about your team ’s experience, this one is more about general trends that affect everyone.

For example, if a tech startup is considering an initial public offering , you’ll review tech IPOs from the past 6-12 months, explain how they’ve performed, and discuss the types of companies that tend to go public.

Here are a few examples of industry updates:

And here are a few examples of deal/transaction updates:

After these first few sections, which are similar in any pitch book, the structure and content start to differ based on what the bank is pitching.

We’ll look at three broad categories here:

- Sell-side mandates (i.e., convince a company to sell itself)

- Buy-side mandates (convince a company to acquire another company)

- Financing mandates (raise debt or equity).

You’ll start by including a few slides on how your bank would position the company and make it attractive to potential buyers.

For example, if the firm is a traditional services provider with a growing online presence, you might attempt to spin it as a “SaaS” (Software-as-a-Service) company – within reason.

If you’re pitching a large company on a divestiture, you might explain how you’ll make the division sound like more of a standalone entity – meaning that buyers won’t have to spend as much time and money integrating it.

Next, you’ll lay out the company’s valuation and the price it might expect to receive in a sale.

This valuation section might be only 1-2 slides in a short pitch book or 20+ slides in a longer one.

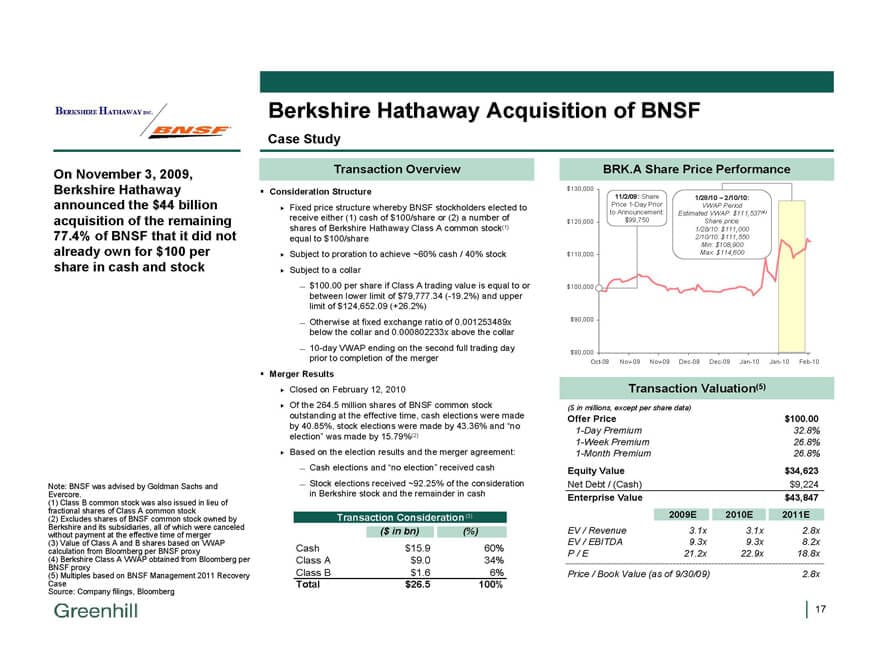

Common elements include the valuation football field , output of a DCF model , comparable public companies , and precedent transactions .

The “football field,” or summary valuation, pages range from simple to more interesting to so complicated they could be eye charts .

Here are a few examples of other valuation-related slides:

It is unusual to include a Contribution Analysis or any M&A analysis in this section unless the deal is highly targeted or has advanced quite far.

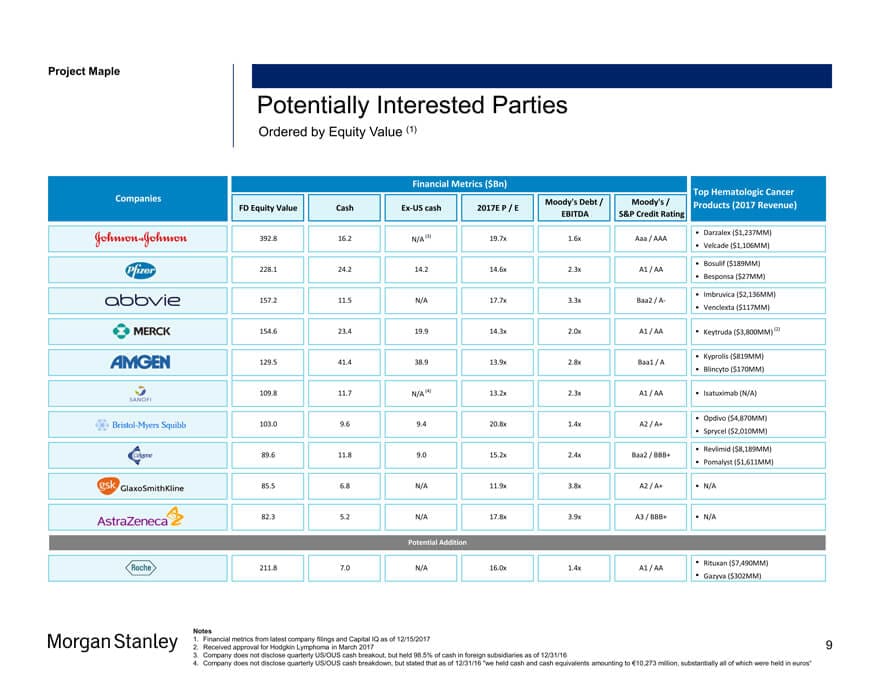

After the valuation section, you’ll discuss “potential buyers,” a list that is sometimes the longest and most time-consuming section of the entire pitch book.

Short summaries aren’t too bad, but if a senior banker wants a full page on each acquirer, you can look forward to a lot of monotonous work gathering the information.

Here are a few shorter examples:

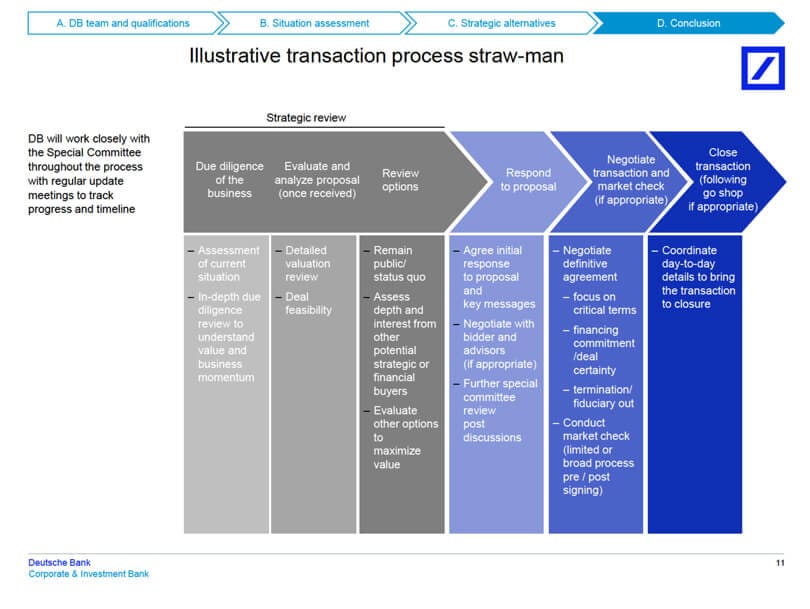

You’ll conclude the pitch book with a summary of your recommendations and the company’s next steps.

For example, you might suggest that the company pursue a targeted sale process with the 5-10 best buyers and aim to complete a deal within 12 months.

These slides tend to be generic ones, used across multiple presentations:

Finally, in longer investment banking pitch books, there is often an Appendix with more detailed models and data, and sometimes even longer lists of potential acquirers.

No one reads this section, but bankers enjoy spending time on unnecessary work (read: evidence of effort).

Investment banking pitch books for buy-side M&A deals follow a similar structure, with a few key differences:

- The “Positioning” part in the beginning might be more about the types of acquisitions the company should pursue and how your bank will help close these deals.

- There may be valuation information, but the purpose will be different: in buy-side deals, you value the buyer to estimate how much a stock issuance to fund the deal might be worth. You might also include quick valuations of potential targets.

- Instead of profiling potential acquirers, you’ll profile potential targets . This list is often longer than the list of potential buyers because a large company could, in theory, choose from hundreds or thousands of potential targets to acquire.

Buy-side M&A pitch books are often shorter than sell-side ones, but they can be more tedious to create due to the longer profile lists.

As a junior banker, you won’t have much input into the acquisition targets that are profiled in these presentations, but senior bankers try to present ideas that:

- Maintain or exceed the firm’s cost of capital.

- Maintain the firm’s competitive advantage.

- Enhance the firm’s ability to serve clients.

- Help the firm expand into high-growth geographies or industries.

Large companies often meet with dozens of bankers per month, so originality can be important as well; many investment banks pitch the same set of acquisition targets repeatedly.

If you present an idea the company has seen 100 times before, they’re unlikely to be excited – but if you find a company they haven’t considered, or you have some exclusive insight, you’ll capture their attention.

It’s tough to find real investment banking pitch books for these transactions because most buy-side M&A deals never close, so the banks do not disclose any of the documents.

But here are a few company profile and associated commentary slides similar to the ones found in buy-side pitch books:

- Brookfield Canada Office Properties by Greenhill

- Banco Santander S.A. by Goldman Sachs

- Side-by-Side Comparison of Buyer and Seller by JP Morgan

- Equity Research Commentary on Buyer’s Offer for Seller by Greenhill

In financing mandates – for equity, debt, and even restructuring deals – there are a few major differences compared with the investment banking pitch books described above:

- No Profiles – You are simply pitching the company on raising capital or restructuring its capital, so there is no need to discuss potential buyers or sellers.

- Financing Models Instead of / or In Addition to Valuation – Valuation still matters for equity and restructuring deals, but you will also have to present additional analyses that are relevant to the deal.

For example, if you’re pitching an IPO, you might show the range of multiples at which the company could go public, the range of proceeds it might receive, and how its value might change after the deal.

In a debt deal, you’ll show the credit stats and ratios for the company under different scenarios, such as Term Loans vs. Subordinated Notes, and explain which one is best based on that.

For more examples, please see the articles on ECM , DCM , and Restructuring .

Also, see our coverage of IPO valuation models and debt vs. equity analysis :

Many other presentations get labeled “pitch books” even if banks pitching their own services do not create them.

For example, management presentations for pitching clients to potential buyers are often labeled “pitch books.”

However, they’re just extended versions of the Confidential Information Memorandum (CIM) .

And in the EMEA region, they’re the same thing because CIMs tend to be more like presentations than written documents.

Banks also create presentations to deliver Fairness Opinions , update clients on recent buyer or seller activity, and update clients on the status of M&A deal negotiations.

None of these is a pitch book according to the classic definition, but the slides often look similar, and there may be some common elements, such as the valuation section.

Not all pitch books take days or weeks to complete – shorter ones might require only a few hours of work.

But they can easily spiral into never-ending projects that require all-nighters and extraordinary effort to finish, resulting in those legendary investment banking hours .

That’s because of:

- Attention to Detail – You’ll spend a lot of time making sure your punctuation is consistent, that all the footnotes are in the right spots, and that the dates are correct.

- Dozens of Revisions – Senior bankers love to make changes well past the point of diminishing returns. It’s not uncommon to see “v44” at the end of file names.

- Conflicting Changes – The Associate wants one thing, the VP wants another, and the MD wants something else. And if you implement the MD’s version based on seniority, the others may fight back.

- Random Graphic Design Work – This one is more of an issue at boutique firms that lack presentations departments, but sometimes you’ll have to spend time creating fancy visual elements on slides – which end up being useless once your MD changes his mind and rips out those slides.

If you’re new to the industry, you should familiarize yourself with the layout and design elements of pitch books, but you do not need to be an expert on the creation process.

Different banks use different tools and methods, so it might be counterproductive to learn too much in advance.

You should also learn the key PowerPoint shortcuts very well, including how to customize PowerPoint to make it more efficient (see our tutorial on PowerPoint Shortcuts in Investment Banking below):

https://www.youtube.com/watch?v=tnJ1e2xJmFc

Everyone knows that Excel is important in finance, but people tend to underestimate PowerPoint – even though most junior bankers spend more time in PowerPoint than Excel.

To learn those efficiently, check out our PowerPoint Pro course , which covers the fundamentals of presentation creation, including how to set up PowerPoint properly in the first place, alignment and formatting tricks, slide organization, pasting in Excel data, and applying the “finishing touches.”

There are also practice exercises for creating deal and company profiles and fixing slides with formatting problems.

If you learn all that and understand the structure and layout of investment banking pitch books, you won’t have much to complain about – even as the other interns and analysts around you are whining.

You might be interested in a detailed tutorial on investment banking PowerPoint shortcuts or this article titled Stock Pitch Guide: How to Pitch a Stock in Interviews and Win Offers .

About the Author

Brian DeChesare is the Founder of Mergers & Inquisitions and Breaking Into Wall Street . In his spare time, he enjoys lifting weights, running, traveling, obsessively watching TV shows, and defeating Sauron.

Free Exclusive Report: 57-page guide with the action plan you need to break into investment banking - how to tell your story, network, craft a winning resume, and dominate your interviews

Read below or Add a comment

10 thoughts on “ Investment Banking Pitch Books: Design, Examples & Templates ”

Hi Brian. Thank you for valuable information!

I’m currently interning. After sitting in a client presentation. What questions should I ask my supervisor regarding the presentation. As we’re going to have a follow up call

I’m not sure I understand your question. The questions you ask are completely dependent on the presentation, so I can’t really answer this without knowing the contents of the presentation.

Its a great article. Appreciate if you also have a link or article for new PE firm Pitch Deck (presenting to investment banks or FIGs), please. Thanks

Sorry, don’t have anything there.

Great article! The information is very helpful and informative. Where and how can I find other examples of sell-side pitchbooks similar to the ones mentioned in this article?

Thanks, Ryan

Thanks. Unfortunately, sell-side pitch books are hard to find because they’re not disclosed publicly. You can find presentations for recently announced deals by Googling the deal’s name and limiting the search to the sec.gov site and going through those results.

Is an information memorandum informally called a teaser or is this something else?

A teaser is a much shorter document, such as a 1-2-page summary of the company’s key benefits, financials, growth opportunities, etc.

Leave a Reply Cancel reply

Your email address will not be published. Required fields are marked *

Perfect Your PowerPoint Skills

The BIWS PowerPoint Pro course gives you everything you need to complete pitch books and presentations in half the time and move straight to the front of the "top tier bonus" line.

Investment banking pitchbook: Types, examples, and tips

A pitchbook is an essential sales tool in the investment banking process . It helps bankers pitch their services to current and potential clients.

The guide below aims to explain how a pitchbook works and how to create it.

What is a pitchbook?

An investment banking pitchbook is a marketing document created and presented by investment banks to existing and potential clients to sell their advisory services.

An investment banking pitchbook is also referred to as a merger and acquisition pitchbook, sell-side pitchbook, or Confidential Information Memorandum. For startups, a pitchbook is typically called a pitch deck.

What is a pitchbook used for?

A pitch, a presentation made using a pitchbook, aims to persuade a potential client company to choose your investment firm to handle a financial transaction like M&A, IPO, restructuring, or raising capital.

Thus, each investment banker wants to make a pitchbook concise, informative, convincing, and attractive enough to attract and win prospective clients.

Note: To learn everything about starting a hedge fund , read our dedicated article.

Types of investment banking pitchbooks

General pitchbook.

General pitchbooks provide an overview of the investment bank. They contain

- General information like the company’s vision, mission, global presence, and key management personnel

- Information on recent deals, including client lists and services provided to them

- Firm’s ranking in comparison with its competitors

- Statistics related to recent deals and successful investments

A general pitchbook should be regularly updated with current information.

Sell-side M&A pitchbooks

When a firm wants to sell its business or a part of it, it turns to investment banks that can help them find potential buyers. Investment bankers, for their part, create sell-side M&A pitchbooks to convince the client to choose them to handle the M&A transaction.

A sell-side M&A pitchbook contains

- A list of potential buyers most suitable to the client’s needs and requirements; if there is no known potential buyer, they may include examples or a generic profile of a potential buyer

- Bank overview highlighting the bank’s main advantages over its competitors

- Valuation overview specifying the value of the company

- Recommendations helpful to the client to complete the transaction successfully

- Appendix including additional details of the deal, potentially interesting to the client

Deal pitchbook

A deal pitch book is created specifically for a particular deal with the purpose to prove that an investment firm can specifically cater to its client’s financial and investing needs. Here’s what it contains:

- Lists of the firm’s major accomplishments and clients

- Graphs that demonstrate the market growth rate, the firm’s positioning overview, and the valuation summary that shows the firm’s potential to serve its client

- Relevant financial models and statistics wherever necessary

- Examples of how the firm might execute the deal . Details depend on the nature of the deal; for instance: for an M&A, a list of potential partners, buyers, or sellers; for an IPO, the profile of investors; for private equity funding, profiles of financial sponsors; etc.

A deal pitch book should be concise and contain the most relevant information to demonstrate how the firm can contribute and help achieve the client’s goals.

Management presentations

After clients settle for a deal with an investment bank, they create a management presentation, aiming to pitch to potential investors. The presentation includes:

- A firm’s main attributes and specific details such as products, services, customers, market overview, key company executives, organizational chart, financial performance, and growth forecasts

- Company’s valuation analysis showing the estimated value or worth of an asset

- Financial strength highlighting the firms’ advantages and arguments to invest

- Investment needs and details about the project that needs to be financed

- Client’s goals and how the investment firm can help achieve them

- Weaknesses and recommendations for improving them

To prepare a management presentation, investment bankers should actively interact with their clients and have regular feedback sessions. Only in such a way a pitch book will be comprehensive and contain sufficient information about the company to attract investors.

Investment banking pitchbook examples

Investment banking pitch publications are difficult to find as they contain confidential information. Consequently, good examples to follow when preparing your presentation are very rare.

A few pitchbook examples have been filed with The Securities and Exchange Commission (SEC) and are now available to the public. Find them below.

- Deutsche Bank pitchbook

Deutsche Bank Securities Inc. is a company offering investment advisory services, such as financial planning, portfolio management, asset allocation, etc. With the presentation, they pitch to AmTrust, a property and casualty insurer, to become their sell-side advisor.

- Perella pitchbook

Perella Weinberg Partners is a financial services firm focused on investment banking advisory services. With the presentation, it pitches to retailer Rue21, evaluating a buyout by private equity firm Apax Partners.

- Goldman Sachs Pitchbook

Goldman, a leading global investment bank, is pitching to Airvana, a mobile broadband company, to become their sell-side advisor. This is a typical sell-side pitchbook that focuses on why the client should choose Goldman for the transaction.

- Dell special committee investment presentation

This is a pitchbook template to be used by investment bankers, designed by Dell, a well-known technology company. It includes a description of the transaction process, perspectives for the client, an overview of financial forecasts, and an evaluation of strategic alternatives.

How to create an investment banking pitchbook

Find out how to create pitchbook presentations.

Who prepares a pitchbook?

The pitchbook preparation involves several contributors—anyone from analysts and associates to senior bankers like a managing director and a vice president.

The VP and the managing director define the structure of the pitch. The outline should be focused on the financial solution required by the client. After that, the outline is given to the associates and analysts. They research, analyze, and propose numbers relevant to the client’s industry.

Before the pitchbook is completely ready for presentation to the clients, it undergoes many changes and drafts. Such a diligent approach ensures there are no mistakes that might compromise the firm’s reputation.

Usually, the whole process takes from a couple of days to a few weeks, depending on how much time the deal team has to devote to creating the pitchbook.

When investment bankers prepare a pitchbook, they need to double-check every detail and ensure they’re using the most up-to-date information and statistics. It demonstrates professionalism and shows clients they can rely on the firm to achieve their financial goals.

What to include in an investment banking pitchbook

Here are the main components of an investment banking pitchbook that aims to win a new client:

Start with the title, logos, and date. Then give a table of contents indicating what the pitchbook consists of.

- Current state overview

State the purpose of the pitchbook—the client is looking for growth and your firm can help with it.

- Bank introduction

Tell about your bank, its achievements in the client’s industry, and why you’re better than competitors. Also, mention people that are going to be involved in the transaction, highlighting their experience and explaining why they are the best for this job.

- Market overview

Describe the market trends in the client’s industry. Use visual aids like charts and graphs to make the pitch book presentation clearer.

- Valuation methods

Show what valuation methods the bank used to determine the worth of the asset. The most common methods are DCF analysis, comparable company analysis, and precedent transactions.

- Transaction strategy

Emphasize key points of the strategy that the bank will use during the transaction—timing, fees, the capital the bank can raise, etc.

Provide the additional information that wasn’t included in the main pitchbook but that the client may need to look at. For example, calculations or financial reports.

How to deliver the pitch

The pitch is usually delivered in person at the bank or client’s office by senior members of the investment banking team. As a rule, it’s the managing director who leads the meeting.

Junior members like analysts or associates may be present but don’t actively participate in the presentation. They can just take notes or look for additional information when required.

Here are a few helpful tips for delivering the pitch:

- Make the presentation engaging and clear

Ensure that everyone can hear and see you well. Also, don’t overdo it with jargon—speak so that everyone can understand you.

- Clarify the opportunities and risks

Describe the opportunities the client will have working with you, but also be honest and straightforward about the challenges the client will face during the transaction. It’s also essential to propose possible solutions to the difficulties.

- Show the change your service will create

Be descriptive and let the client feel the positive change they’re going to experience if working with you.

- Answer the questions

Be ready to deal with different questions, including uncomfortable ones. Make sure to return to the client with the answer, in case you don’t have it at that moment.

- Explain why you and not someone else

Give the client something that makes you unique and attractive to them as they have probably heard other pitches very similar to yours.

Key takeaways

Here are the main points to remember about an investment banking pitchbook:

- An investment banking pitchbook is a document or presentation created by an investment bank and then used by its sales department to sell products and services to attract new clients.

- The main investment banking pitchbooks are general, sell-side M&A, deal pitchbooks, and management presentations.

- A pitchbook is prepared by a managing director, a vice president, analysts, and associates.

- The main components of an investment banking pitchbook are the intro, current state overview, bank introduction, market overview, valuation methods, transaction strategy, and appendix.

Other insights

M&A payment methods: Cash vs. stock explained

Privacy Overview

- The Investment Banker Micro-degree

- The Project Financier Micro-degree

- The Private Equity Associate Micro-degree

- The Research Analyst Micro-degree

- The Portfolio Manager Micro-degree

- The Restructurer Micro-degree

- Fundamental Series

- Asset Management

- Markets and Products

- Corporate Finance

- Mergers & Acquisitions

- Financial Statement Analysis

- Private Equity

- Financial Modeling

- Try for free

- Pricing Full access for individuals and teams

- View all plans

- Public Courses

- Investment Banking

- Investment Research

- Equity Research

- Professional Development for Finance

- Commercial Banking

- Data Analysis

- Team Training

- Felix Continued education, eLearning, and financial data analysis all in one subscription

- Learn more about felix

- Publications

- Online Courses

- Classroom Courses

- My Store Account

- Learning with Financial Edge

- Certification

- Masters in Investment Banking MSc

- Find out more

- Diversity and Inclusion

- The Investment banker

- The Private Equity

- The Portfolio manager

- The real estate analyst

- The credit analyst

- Felix: Learn online

- Masters Degree

- Public courses

Investment Banking Pitch Book

By Ivy Wang |

Reviewed By Rebecca Baldridge |

February 14, 2023

What is an Investment Banking Pitch Book

In investment banking, a pitch book is a marketing presentation intended to convince an existing or potential client to retain their firm for a deal. Pitch books typically contain sections on the merits of the transaction, an analysis of potential buyers or sellers, pricing and valuation information, and key risks to mitigate.

A well-tailored pitch book is a secret to bagging multi-million-dollar deals. Investment banking analysts and associates spend a significant amount of time working on pitch books, and any career in investment banking requires the ability to create pitch books and use them to pitch to prospective investors.

Key Learning Points

- Investment banks create pitch books to market their business to clients. The goal is to be chosen by the client to handle a transaction such as buying or selling a company or raising capital.

- A pitch book for an M&A transaction includes the target’s vision, mission, company overview, and business model.

- Most investment banking pitch books are created in PowerPoint and fall into three categories: bank introductions, deal pitches, and management presentations.

- Creating an investment banking pitch book requires significant preparation and meticulous attention to detail.

Types of Investment Banking Pitch books

There are several types of investment banking pitch books, differentiated depending on purpose and content. We can categorize them as one of three types:

- Market Overviews/Bank Introduction: These are the pitch books used to introduce a bank to prospective clients. They can also be used to give clients updates. These decks include Information that will help create a favorable impression for potential clients, such as background and history, vision and mission, organizational structure, company size, recent achievements and successful deals, and a market overview/update.

- Deal Pitch Book: These include two main types, which are buy-side and sell-side M&A pitchbooks. Debt insurance and IPOs also fall under this category. These decks include details that will present the deal and help potential clients understand how a bank proposes to undertake the work. This might include the following: market growth rate, relevant financial models , list of potential buyers, acquisition candidates, and financial sponsors with detailed descriptions (if applicable).

- Management Presentations: These presentations are used to pitch clients to investors after the business is won. Important information about the client company is included, such as background, market overview, products and services, customers, organizational chart, financial performance, and expansion and growth opportunities.

Uses of Pitch Books

A pitch book is one of the most important tools that investment bankers use to help sell their services:

- It acts as a marketing device and is used by all the investment banks worldwide.

- It exemplifies valuable and comprehensive marketing material.

- It acts as the starting point of the initial pitch or sales introduction for the investment bank when it is trying to seek new business.

- It provides a deep analysis of a current or potential client and deal.

- It offers the bank a chance to demonstrate why a client should choose them from a broad field of competitors.

An Inside Look at Investment Banking Pitch Books

In general, a pitch book is divided into 5 sections:

- Market Update – Provides charts illustrating current capital markets conditions. This is the part of the pitch book that is intended to convince clients that now is the right time to carry out a transaction.

- Credentials – Numerous biographies and league tables that show why the bank is the right choice.

- Deal Outline – Gives a sense of what the deal would involve. It also provides other options to consider.

- Considerations – Includes charts and tables exhibiting effects on EPS and any other potential problems. It’s important to read the footnotes in this section as potential problems are normally referred to as “execution” or “management”.

- Appendix –This is a very important section as it includes models with a variety of scenarios.

How to Create a Pitch Book in Investment Banking

Creating an investment banking pitch book can be daunting. It requires careful preparation and attention to detail. Usually, the majority of the pages (especially in the Credentials and Market Update sections) can be lifted from an already-existing book with the names and financials changed.

Almost all investment banking pitch books use a structure similar to the following:

- Situation, or “Current State”: Your prospective client is looking for growth.

- Complication, or “Problem”: The potential client’s growth rate has been slowing.

- Hypothesis, or “Solution”: Acquiring a growing company can meet the potential client’s need for growth.

Then, the deck goes into detail, showing why the hypothesis might be true – including why the bank’s team is qualified to lead the transaction, similar transactions the bank has led before, and the valuation this company can expect to receive.

Pitch books must be designed to impress prospective clients. Apart from the design, they must have a compelling message. It is therefore vital to have a clear message underpinning the pitch. There should also be a clear message on each slide.

Pitchbook Examples

You can learn a lot by looking at examples of pitch books that have been used successfully in the past. They will illustrate what kind of content and design elements work well with investors and potential clients.

Example 1: Goldman Sachs Pitchbook Airvana Go Private Deck

Goldman Sachs has a track record of creating successful pitchbooks. One of their pitch books was used to win Airvana’s business. In the investment presentation, they gave the company the codename Atlas. Goldman made the presentation to Atlas’ Special Committee, and they included many detailed company projections. This shows how fully they understood Airvana’s business and financial position. Goldman included a detailed analysis of several strategic alternatives in their pitchbook.

Example 2: Medley Management’s 3-way Merger with Medley Capital and Sierra Income

This is another excellent example. The pitchbook was prepared by Barclays when they were pitching to become the M&A advisor to Medley Management during its merger with Medley Capital and Sierra Income. It’s a 38 pager that features beautifully designed graphs, pie charts, and tables. These techniques and presentation styles made it easier for Barclays to communicate with its potential clients effectively.

Example 3: Sale of Rouse Properties to Brookfield Asset Management

This is a sell-side pitchbook prepared by Bank of America and presented to Rouse Properties. Brookfield later acquired the business. The presentation includes 58 slides and has an impressive, concise, and detailed executive summary.

Pitchbook Template

The purpose of the pitch book is to give a comprehensive overview of the investment bank. It contains details such as the number of analysts, previous IPO successes, and the average number of deals completed per year. It can also include information about the financial strengths of the bank and the range of services it offers to its clients.

Creating a pitch book is often time-consuming and challenging, but the process can be simplified by using a template. A pitch book template is a blueprint that contains layouts, colors, fonts, effects, background styles, and general content.

Get our free download of an outline of an investment banking pitch book

An investment banking pitch book is a structured PowerPoint presentation created to attract new businesses. The pitch describes why the bank is the best choice for a transaction. The deck would focus on products if used by an investment firm. For example, it could use graphs and comparisons to a suitable benchmark to demonstrate the merits of a portfolio. There isn’t one formulaic way to make an investment banking pitch book. Much of the work depends on various factors, such as company culture or who a bank is pitching to.

If you want to get the same training as new hires to the top 4 investment banks, and master accounting, financial modeling, valuation, plus M&A and LBO analysis, enroll on the Investment Banker online course .

Additional Resources

Investment Banking Course

Everything You Need to Know about Investment Banking Spring Weeks

Investment Banking Recruitment: The Ultimate Guide

Investment Banking Interview Skills

Share this article

Investment banking pitchbook template and workflow.

Sign up to access your free download and get new article notifications, exclusive offers and more.

Recommended Course

Access average EBITDA and revenue purchase multiples for private middle market companies across 11 industries. Learn More.

M&a process: a step-by-step guide.

- Mergers & Acquisitions

- Aerospace, Defense, Government & Security

- Building Products & Construction Services

- Business Services

- Education & Training

- Energy, Power & Infrastructure

- FinTech & Financial Services

- Industrial Technology

- Industrials

- Technology, Media & Telecom

- Transportation & Logistics

Having a thorough M&A Process can help increase your chances of success and elevate shareholder value.

Whether you’re looking to retire or start a new venture, you might be inching closer to selling your company. In theory, it’s simple: find a buyer and complete the deal. Unfortunately, it’s never that straightforward to launch a Mergers and Acquisitions (M&A) process, with numerous factors to consider when deciding to sell your business. Common questions that we’ve received include:

- Is now the right time to sell my business?

- What type of buyer is the best for my company?

- How can we ensure maximum value for our shareholders?

- What does the M&A process even look like?

While the first three questions require an in-depth, personal conversation between you and your investment banking advisor, the final question is a bit more straightforward. Below is an outline of the complex 6-9 month M&A process that Capstone Partners Investment Banking Teams use to facilitate transactions and maximize the value of our clients’ companies.

Phase 1: Preparation and Planning

The first step in the M&A process is to gather information on your company so that your advisor can effectively represent you in front of buyers. This information highlights your history, products/services, supply chain and distribution networks, customer base, sales and marketing strategies, growth potential, management structure, competitive landscape, and, last but certainly not least, financial performance. You’ll need to gather information and be readily available to respond to your advisor’s additional requests and inquiries. Expect this stage to be one of the more time intensive for you.

Using the information that you have provided, your advisor drafts the Confidential Information Memorandum (CIM) – an in-depth report detailing precise market positioning, company history and milestones, basic financial information, company structure, products, and more. From the CIM your advisor creates a one-page high-level overview of your company that is used as a Marketing Teaser to generate initial interest in your company while maintaining anonymity. The teaser will be sent to companies that you and your advisor have identified as potential buyers. These target companies are required to sign and return a Non-Disclosure Agreement (NDA) prior to receiving the full CIM (which can easily reach 50 pages in length).

Phase 2: Marketing

During this phase, your advisor contacts buyers and gauges their interest by emailing the teaser and following up with calls and emails to address any questions.

Upon receipt of the NDAs, your advisor distributes the CIM to provide expanded company information and transaction objectives. Generally, expect two weeks for buyers to review the CIM and express interest. In the meantime, your advisor will track the process while answering appropriate questions and responding to supplemental information requests that may arise during review.

Phase 3: Qualification and Refinement

At this stage in the process, your advisor begins to receive preliminary Indications of Interest (IOI) from prospective buyers. An IOI is a potential buyer’s non-binding offer where they provide a valuation range, sources of financing, anticipated timeline for due diligence to be conducted, structure of the transaction, and a plan for post-transaction organizational and operational structure.

The goal is to receive multiple IOIs and establish a competitive landscape that will drive the valuation and terms in your favor. While pricing will be a primary factor when comparing IOIs, it’s also important to consider cultural fit, ability to complete a transaction, buyer reputation and sources of funding.

Taking into consideration all IOIs and potential buyers, you and your advisor review terms together and select a short list of companies to invite to management presentations. Having a targeted, highly manageable short-list is paramount, as it will lead to efficient final stages of the vetting process. Moving forward, your advisor schedules visits, helps create management presentation materials, and coaches you for the meetings themselves.

Phase 4: Selection and Structuring

The selection and structuring phase of the process begins with the management presentations. Most often, Capstone’s clients opt for an off-site location for the meetings to maintain a confidential process. For the first time, you meet with potential buyers to introduce your management team, provide company information, communicate transaction goals, and position your company as a “can’t-miss” investment opportunity. Additionally, the in-person presentations allow both you and the potential buyers to vet each other, professionally and personally.

Upon the completion of management visits, interested buyers submit a Letter of Intent (LOI) which simply sets forth the framework for a deal including a specific purchase price, closing date, sources of funding, length of exclusivity and additional terms that are pertinent to the deal.

Carefully considering all elements of the LOIs, you must select one company to move forward with. Though both sides can still step away from the deal, the signed LOI establishes a period of exclusivity during which neither party can engage with other firms. Agreeing to the period of exclusivity demonstrates a good faith understanding as the buyer will be investing significant resources into due diligence (lawyers, accountants, time, etc.) and wants to be certain that you are not actively shopping the deal to anyone else.

Phase 5: Due Diligence

With the period of exclusivity in effect, both parties conduct their final due diligence efforts. During this phase, you can expect the potential buyer to be far more meticulous in analyzing all aspects of your business including financial records, physical infrastructure, human capital, customer concentration, products and services, growth potential and competitive landscape. Your advisor monitors all progress, addresses any concerns and prepares final ad hoc information as may be requested. Meanwhile, your advisor also conducts due diligence on the buyer to confirm management fit and ability to close the deal. According to a recent Forbes article , “Even a deal that makes strategic sense can come awry if those involved have not done proper due diligence — including the increasingly important assessment of what divestments might need to be made to meet regulatory concerns — or carried out the ground work required to get a deal done.”

Phase 6: Final Negotiations and Closing

Pending a successful due diligence phase, both parties and their respective legal teams resolve all price, structural and technical discrepancies in final negotiations. Concurrently, you and your advisor craft a communications plan to address employees, stakeholders and the outside community. Once all documentation and communications are in order, you and the buyer coordinate the closing and execute the wire transfer. This completes the extensive M&A process.

Pre-planning for the M&A Process: Essential Questions to Answer

Before jumping into the specifics of the M&A process, there is a pre-planning process that needs to occur. This is mission-critical. Questions, such as those that were touched on at the beginning of this article, and those below need to be asked and answered in order to prepare for the M&A process and for what comes after.

- What is the next step in my professional career?

- What are my priorities with the process?

- How will I manage the liquidity that will result from this deal?

An experienced investment banking advisor can help walk you through these questions and more, ensuring you have thoroughly considered all of your options to meet your goals and increase the probability of a sale, your speed to closure, and get you the maximum valuation for your company. If you’re thinking about considering an M&A transaction within the next 24 months and would like some advice on how to start the process feel free to contact us for advice here .

Related Insights

Advantages and disadvantages of debt financing.

- Debt Capital Advisory

- Equity Capital Advisory

Construction Services Market Update – May 2024

- Construction Professional Services

Women Entrepreneurs Report

Insights for middle market leaders.

Receive email updates with our proprietary data, reports, and insights as they’re published for the industries that matter to you most.

- Recently Active

- Top Discussions

- Best Content

By Industry

- Investment Banking

- Private Equity

- Hedge Funds

- Real Estate

- Venture Capital

- Asset Management

- Equity Research

- Investing, Markets Forum

- Business School

- Fashion Advice

- Technical Skills

- Valuation Resources

Roadshow Presentation

A part of a series of presentations or sales pitches

Currently an investment analyst focused on the TMT sector at 1818 Partners (a New York Based Hedge Fund), Sid previously worked in private equity at BV Investment Partners and BBH Capital Partners and prior to that in investment banking at UBS.

Sid holds a BS from The Tepper School of Business at Carnegie Mellon.

Prior to joining UBS as an Investment Banker, Himanshu worked as an Investment Associate for Exin Capital Partners Limited, participating in all aspects of the investment process, including identifying new investment opportunities, detailed due diligence, financial modeling & LBO valuation and presenting investment recommendations internally.

Himanshu holds an MBA in Finance from the Indian Institute of Management and a Bachelor of Engineering from Netaji Subhas Institute of Technology.

- What Is A Roadshow Presentation?

- What Is Covered In A Roadshow Presentation?

Post-Roadshow Process

What is a roadshow presentation.

A roadshow presentation is a part of a series of presentations or sales pitches done by a company’s management and/or the underwriting investment bank prior to conducting an initial public offering (IPO).

When a company is choosing to raise capital via an IPO, the company's management team and, at times, the advising investment bank, will meet with institutional investors to build up the order book for the offering.

The order book contains large volume offers from financial institutions such as hedge funds or pension funds on the security, which help aid in the proper pricing of the IPO further down the line.

The roadshow presentation is of paramount importance in the IPO process as institutional investors make up a large portion of the number of shares purchased. Thus, a successful roadshow presentation series can make or break an IPO.

Roadshow presentations most often occur in large cities such as:

- Los Angeles

- San Francisco

The process, on average, takes about three weeks, with a mix of different meeting styles.

Large “ blue chip ” investors typically garner one on one meetings while other highly important institutions will have small group meetings or large group meetings such as a luncheon.

Roadshow presentations contain an immense amount of information pertaining to the business, its management, its past, and its future outlook.

Key Takeaways

- Roadshow presentations are sales pitches done by companies pursuing an IPO

- These presentations are done to entice institutional investors and spark demand for the offering

- The presentation contains a management overview, the business’ key drivers and growth opportunities, a financial overview and projections, and a “sales story”

What is Covered in a Roadshow Presentation?

It has pretty standard core topics that need to be addressed to ensure that a successful “hit rate” is achieved and demand for the offering is cultivated. Typically, they start off with an introduction of the company's management team and C-suite executives.

The presentation should also have an in-depth look into their earnings and overall financials. Another vital section is their recent past, current, and future outlook on key drivers of the business. This typically includes data and projections on items such as sales or revenue.

Additionally, over the IPO process , the company and its advisors craft a story to sell to investors on the company, about:

- Growth prospects of the company

- Competitive advantages

- The reasons why it should receive investors’ capital

This is also thoroughly covered in the presentation.

The details of the offering itself are a topic of discussion, including the size of the offering and IPO stock price target. Investors attending roadshows have the opportunity to then make offers in a few different ways.

Investors can place stock orders.

Example: 2,000 shares at a price of $20

Or they can place limit orders in which there is a cap on the price paid per share

Example: 2,000 shares at a price per share of no more than $18

Everything You Need To Master PowerPoint for Finance

To Help You Thrive in the Most Prestigious Jobs on Wall Street.

After the roadshow presentation series is complete, there is still much work to be done before the successful launching of an IPO .

The underwriting investment bank follows the roadshow presentations, collecting all the offers from the order book and analyzing the supply/demand dynamics of the offering. This analysis helps further educate the team on selecting the optimal IPO price.

After the conclusion of this analysis, a final prospectus is drafted, reviewed, edited, and published. This final prospectus is then used to further advertise the offering to potential investors.

The prospectus is also sent to the Securities and Exchange Commission ( SEC ) for approval. Following SEC approval, the offering date and price per share are set and ready for launch.

When the IPO day comes, the shares begin trading at the designated price at the beginning of the trading day.

Oftentimes, initial public offerings will have great price appreciation in the first few days or weeks of trading, as the pent-up anticipation enhances demand.

The funds received from the sale of the predetermined number of shares are then obtained by the issuing company.

Following the IPO, the company may be able to engage in follow-up offerings, which can sometimes involve a similar roadshow presentation process to the IPO.

Initial public offerings are a key way for businesses to grow and scale their operations through the funds received from selling an equity stake in the company. The roadshow presentation is a key step along the road to a successful IPO and can be the deciding factor in whether or not its goals are met.

Everything You Need To Master Valuation Modeling

Researched and authored by Charlie Fair l LinkedIn

Reviewed and edited by James Fazeli-Sinaki | LinkedIn

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

- EV/EBIT Ratio

- Free Cash Flow (FCF)

- Gordon Growth Model

- Owner's Equity

Get instant access to lessons taught by experienced private equity pros and bulge bracket investment bankers including financial statement modeling, DCF, M&A, LBO, Comps and Excel Modeling.

or Want to Sign up with your social account?

Table of Contents

- --> What Does--> --> --> --> table of contents--> <--.

- --> What--> -->